In the short-term it looks as though the combination of the impact of bushfires and COVID-19 will put the brakes on the Australian economy

17 February 2020 | Shane Oliver, AMP Capital

The number of confirmed COVID-19 cases in China spiked over the last week, after Hubei province added patients confirmed via clinical tests (CT imaging scans) but who have tested negative via lab tests (nucleic acid testing).

There are issues with both testing methods – the lab tests are slower and can sometimes give false negative results whereas CT scans may just be revealing conventional pneumonia. It could be a case of China front loading some bad news after it replaced some top officials in Hubei and WHO has stuck to reporting only lab confirmed cases.

On the basis of the latter there is still some evidence of a downtrend in the number of daily new cases. And this would likely also be the case if the clinically diagnosed cases are spread back over the last few weeks for which they relate to.

Of course, there is a lot of uncertainty around this and it may become clearer as WHO becomes more involved on the ground in China in the week ahead.

There’s been no alarming change in the COVID-19 situation

More broadly though the picture is little changed: 99% of cases are still in China; 80% of these are in Hubei province; the transmission of cases outside China beyond the cruise ship in Japan remains low and the mortality rate is just over 2% and mainly relates to older people with pre-existing conditions.

The key to watch remains the number of daily new cases and the spread of cases outside China – although in terms of the former this is being made difficult at present by volatility in the number of cases, it’s worth noting that this is not unusual in the case of virus outbreaks.

Although, there is much uncertainty our assessment remains that the most likely scenario with 75% probability is that the virus will be contained in the next month or so.

However, with many Chinese staying at home as confirmed by various indicators around transport congestion, coal consumption and property sales the hit to Chinese growth and the flow on to the global growth will be big this quarter. In fact, it’s conceivable that global growth will be zero in the March quarter.

Rough estimates suggest that 30% of China’s population and 50% of its GDP is quarantined and each week this remains the case will knock 1% off Chinese GDP and nearly 0.2% directly off global GDP. however, if the outbreak is contained in the next month or so as we expect then growth will bounce back in the June quarter and shares will largely look through it.

Australian economy bracing for impact of one-off events

For Australia, our assessment remains that the combination of the drag from the bushfires and COVID-19 will detract around 0.6% from March quarter GDP which will see the economy go backwards by around – 0.1%.

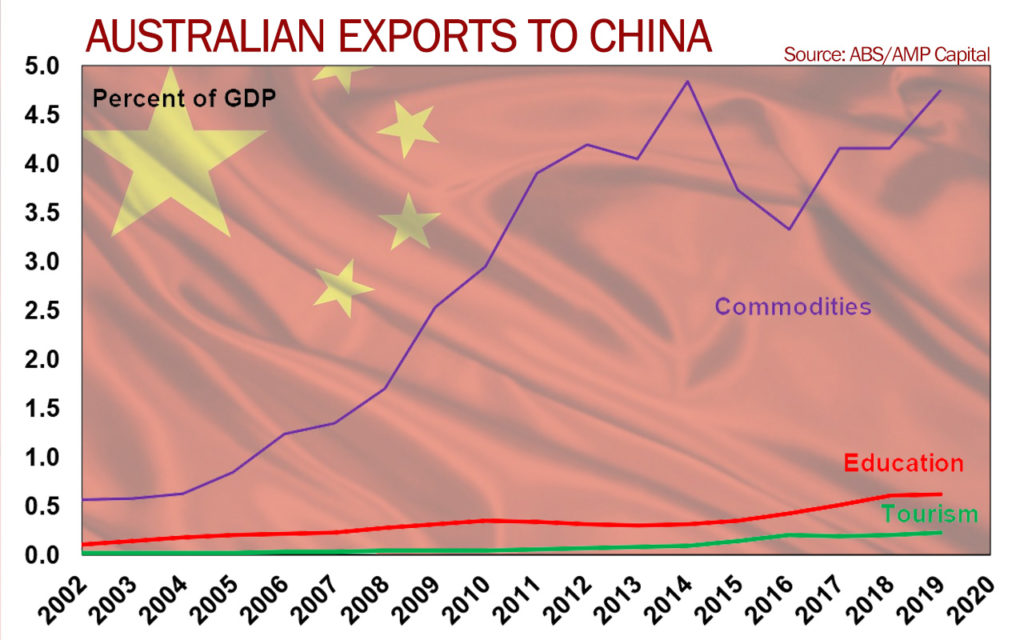

Growth should rebound in the June quarter as the rebuilding from the bushfires kicks in and if as we expect the COVID-19 outbreak is soon contained. The broader vulnerability of the Australian economy should the outbreak drag on though is highlighted by the above chart which shows that Chinese tourists account for 0.2% of Australia’s GDP, Chinese students account for 0.6% and commodity exports to China account for nearly 4.8%, all of which are well up from where they were at the time of the SARS outbreak back in 2003.

Global equities move ahead

Share markets generally rose over the last week, but gains were constrained by ongoing concerns about the COVID-19 outbreak after China announced a large increase in new cases. US shares rose 1.6%, Eurozone shares rose 1.4% and Chinese shares gained 2.3%, but Japanese shares fell 0.6%.

Reflecting the generally positive global lead Australian shares rose 1.5% leaving them just below their January record high with strong gains in financials, utilities, health and consumer discretionary stocks offsetting COVID-19 related weakness in resources stocks. Bond yields were little changed but oil, metal and iron ore prices rose and the Australian dollar rose from its lowest level since 2009.

It’s early days in the December half profit reporting season as only about a quarter of major companies have reported. So far results have been a bit mixed. 61% of companies have seen their profits rise from a year ago but this is below the long term norm of 65%.

Half of the results so far have surprised on the downside which compares to a norm of just 26%, and only 52% of companies have raised their dividends which is well down from the 77% of companies raising their dividends back in August 2018.

Australian housing finance bounces back

Meanwhile, housing finance rose again in December led by owner occupiers and is now up 20% from its mid-year low providing further confirmation of the upswing in the property market.

Of course, this is yet to really boost the housing credit data which relates to the stock of debt because new lending is being offset by the rapid paydown of existing debt, but it likely will start to in the months ahead.

Dr Shane Oliver is Head of Investment Strategy and Chief Economist of AMP Capital