Despite hopes for a recovery, the beleaguered Swiss luxury watch industry declined further in 1H 2024, according to data from the Federation of the Swiss Watch Industry.

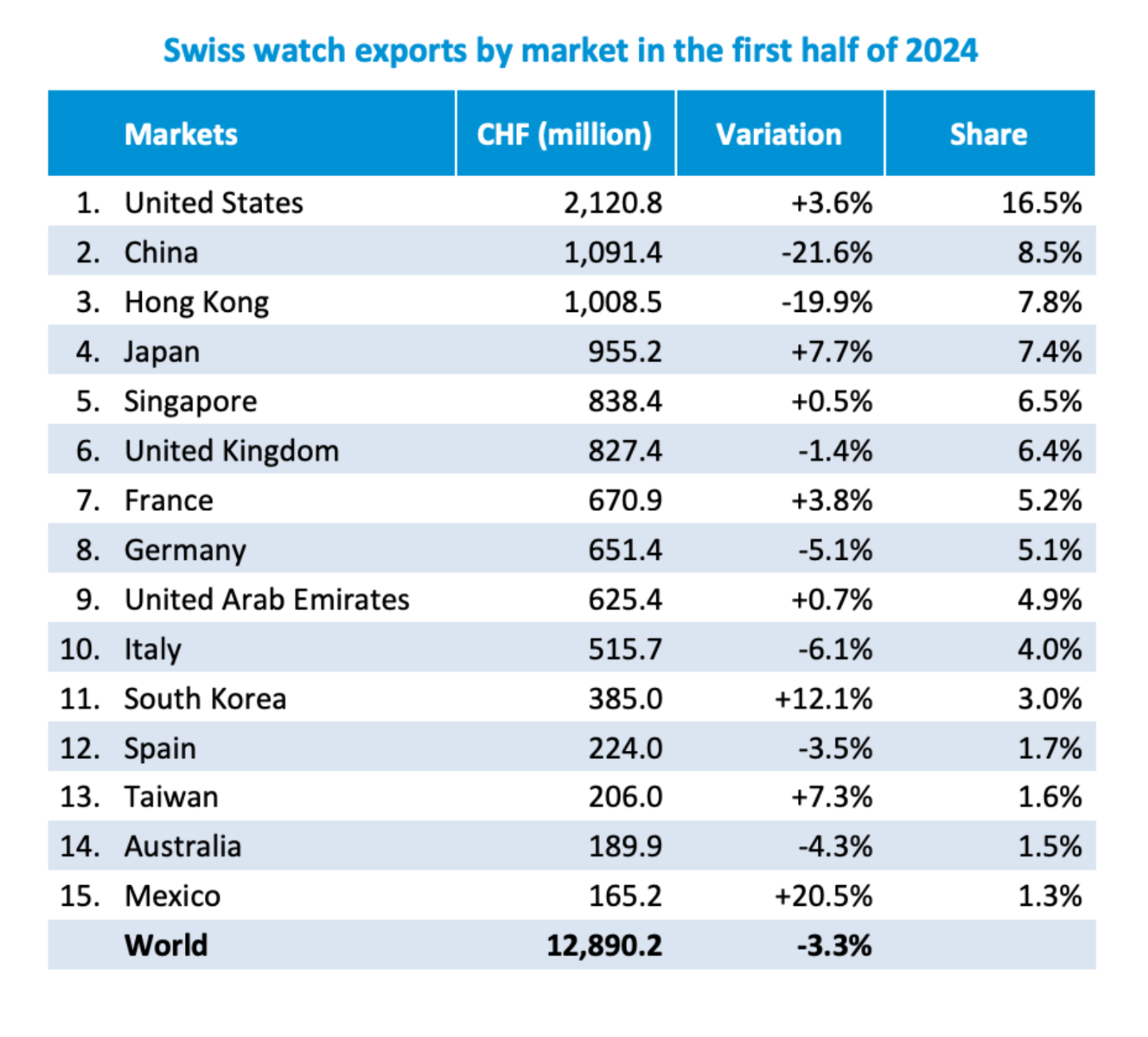

A much-needed turnaround for the beleaguered Swiss luxury watch industry failed to materialize in June. The latest figures released by the Federation of the Swiss Watch Industry indicated a further decline – in 1H 2024, Swiss watch exports dropped 3.3% YoY to 12.9 billion Swiss francs ($14.6 billion).

After three years of rapid post-pandemic growth, a dip in demand had been anticipated, but the rate of decline, especially in the Greater China market, casts a shadow over the category’s mid-term prospects.

Demand for high-end Swiss watches in China has been crimped this year as consumers decrease or defer discretionary spending amid decelerating economic growth, high youth unemployment, and a teetering real estate market – or make big-ticket purchases in Japan. As a luxury category, watches also face competition from segments such as leather goods and jewelry, which are less affected by the slowdown.

A two-speed market

Swiss watchmaking, like the rest of the luxury goods sector, operated at two different speeds in the first half of 2024. Exports to mainland China declined 21.6% YoY, while exports to Hong Kong dropped 19.9%. Meanwhile, the rest of the world posted a modest growth of 1%, aligning with the high-level consolidation expected for the sector this year.

Notably, the China market drop was almost exclusively due to the 500-3,000 Swiss franc ($545-$3,270) segment, which represents only 15% of export turnover but plummeted by 19%. Exports of watches priced at less than 500 Swiss francs ($563) fell by 7%, while those over CHF 3,000 ($3,380) performed slightly better than last year, increasing by 0.7%.

Exports to Asia fell 7% YoY, attributable to the Greater China decline. Other main Asian markets produced mixed results: Japan (+7.7%), South Korea (+12.1%), Taiwan (+7.3%), Singapore (+0.5%), and the United Arab Emirates (+0.7%).

Exports to Europe declined 1.1%. The UK’s performance (-1.4%) set the tone, with Germany (-5.1%), Italy (-6.1%), and Spain (-3.5%) losing ground. France was a rare bright spot, benefiting from the Olympic Games effect that helped exports increase 3.8%.

The Americas, driven by the US, achieved growth of 3.8% despite a high comparison base. This strong performance helped the US strengthen its position as the leading market for Swiss watch exports.

Another year of weakness?

Analyst Oliver Müller estimates that the Greater China luxury watch market will demonstrate declining demand and growth until mid-2025, while the US will remain the top global market for at least the next two years.

He notes that Greater China may have delivered “El Dorado growth with minimal effort from the watch brands” over the past two decades, but that such rapid growth is unsustainable in the long term.

“Any brand should have understood by now that it needs to reduce its dependency on the Chinese market,” he adds.

Indeed, Omega and Vacheron Constantin have gradually reduced their dependence on China over the past eight years to focus on other markets. According to a Morgan Stanley and LuxeConsult watch industry report released earlier this year, since 2017, Vacheron Constantin has seen the ratio of Chinese sales versus total sales decrease from 50% to 30%. The brand has prioritized the US in a strategic move that worked in its favor. For the first time in Vacheron Constantin’s history, its sales exceeded CHF 1 billion Swiss francs ($1.12 billion) in 2023.

Despite the discouraging market sentiment and ongoing economic concerns in China, some popular Swiss watch brands remain eager to expand in the market. Currently, Greater China generates only 10% to 15% of Hublot’s global sales.

Still, growth in the region is important for Hublot, “because the average price of Hublot watches sold in Greater China is the highest among all our markets,” Ricardo Guadalupe, CEO of Hublot, told Jing Daily earlier this month. The brand’s higher-priced Big Bang and ceramic watches perform well in Greater China, whereas entry-level watches are more popular in the US, Hublot’s biggest market.

Hublot started establishing its retail network in the US, mainland China, and Hong Kong around the same time, between 2009 and 2010. Since then, the brand has expanded more rapidly in the US, where it has 58 points of sale, compared to 16 in mainland China and 18 in Hong Kong.

“This is because we entered China later than other brands, thus losing out on prime retail space,” Guadalupe says, adding that the brand will not open any new boutiques in mainland China this year, but plans to host pop-ups.

Although China remains one of the leading markets for the luxury watch industry, some fundamental barriers limit its growth potential. According to luxury watch industry analyst Müller, the Chinese government needs to lower import duties if the Swiss watch industry is to capture an even bigger part of Chinese luxury spending.

However, Müller says, “if you read what their official standpoint is on luxury overall, it is clearly not a primary goal.”

By Avery Booker, this article was first published at JING DAILY (Image supplied)