Historically September is a month for market corrections, just like the coronavirus and the race for the White House, this one may not be over yet

20 September 2020 | Shane Oliver, AMP Capital (Image: Jay Clark)

September is often the month for corrections and we have seen a bit of that so far this month with the stretched US market having a top to bottom pullback of 7%, led by the very stretched Nasdaq which has seen a 10% top to bottom fall.

In the process Australian shares have also pulled back 5% but Eurozone and Japanese shares have been little affected. The pullback has relieved overbought conditions while at the same time the resilience of credit spreads, metal prices and growth currencies like the $A tell us its likely just a correction and not the start of a renewed bear market.

Strengthening economic data and very dovish central banks should underpin share markets on a 6 to 12 months horizon, providing coronavirus is controlled. But right now it’s still too early to say the correction is over – seasonal weakness often continues into October, coronavirus could have a third wave into the northern winter, uncertainty remains around the next round of fiscal stimulus in the US and the US election is likely to add to volatility.

Global share markets mostly fall

While shares initially rallied on the back of reasonable economic data, anticipation of Fed dovishness, positive vaccine news and M&A activity, the gains were given up later in the week as tech stocks came under renewed pressure and the Fed did less than some had hoped.

US shares fell 0.6% for their third week of decline in a row, Eurozone shares lost 0.5% and Japanese shares fell 0.2% but Chinese shares rose 2.4%. Australian shares managed a small gain of 0.1% over the week after two weeks of falls with strong gains in resource, property and IT stocks offsetting weakness in financials.

Bond yields rose slightly in the US but fell elsewhere. The iron ore price fell, but metal and oil prices rose as the $US fell, but the $A was little changed.

The lower level of fatalities and absence of a return to a hard lockdown has seen economic recovery continue in most developed countries. However, our US Economic Activity Tracker had a setback over the last week with declines in restaurant and hotel bookings and mobility indicators.

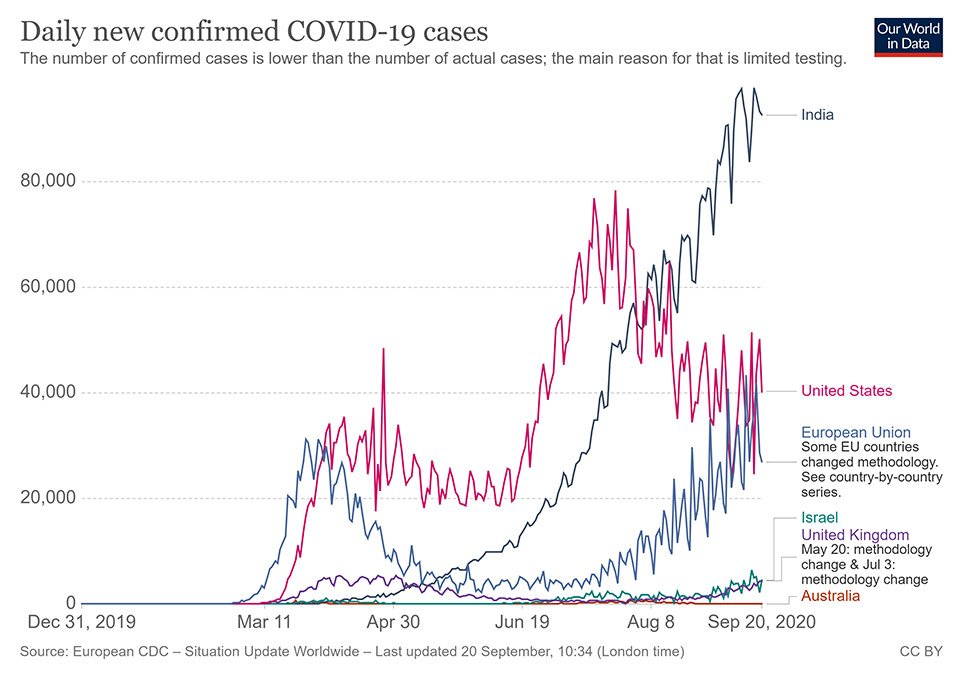

Global second wave

Fortunately, the second wave of new coronavirus cases in developed countries has continued to be far less deadly than the first wave with deaths running well below their April high whereas new cases have been well above.

This reflects a combination of more testing (picking up more younger people), better treatments and better protection for older people. This in turn is continuing to help avoid a return to generalised lockdowns in most countries (Israel and Victoria excepted) – in favour of targeted measures – and helping confidence hold up. Although Europe is at risk here.

The uptick reflects both emerging countries (particularly India) but also developed countries moving up again as new cases in Europe continue to trend up to be now above March/April highs and the US has hooked up again over the last few days (mainly in the south and mid-west).

Australia’s COVID-19 situation improves

And now with new cases sliding, deaths have also fallen sharply in Victoria. While the second wave proved more deadly than the first in Australia in contrast to other developed countries, coronavirus deaths per million people in Australia remain low at 33 compared to the US at 602, the UK at 627 and France at 423.

The decline in new cases has seen our Australian Economic Activity Tracker hook up from August lows but it had a set back over the last week with falls in restaurant bookings and shopper traffic. Expect a rising trend though as Victoria moves to a gradual reopening and other states continue to recover.

RBA aligns with economic “Team Australia”

We expect further easing by the RBA possibly at its next meeting so as to present a united “Team Australia” front with the Federal Government as it’s the same day as the Budget. Further RBA easing is likely to involve a combination of cutting the cash rate and the three year bond yield target to 0.1%, tweaking forward guidance to not raise the cash rate until full employment is reached and inflation is sustainably within the 2-3% target band and possibly adopting a more traditional quantitative easing program.

While other Anglo central banks – namely the RBNZ and the BoE – are now considering negative interest rates we remain of the view that the RBA will continue to avoid going down this path, particularly with RBA research indicating that it can get a bigger impact via other measures than further cuts in the cash rate.

Strong jobs data

August jobs data was much stronger than expected in Australia with employment up by 111,000 which in turn pushed unemployment down to 6.8% (from 7.5%), but it was not quite so strong beneath the surface.

The good news is that just over half the jobs lost in April and May have been returned, effective unemployment which assumes a constant participation rate since March and adds back in those on zero hours has fallen from a high of 14.9% in April to now 9.5% and a loss of jobs and hours worked in Victoria has been offset by strength in other states.

However, the bad news is that the recovery in jobs has been skewed to part-time jobs with nearly 80% reinstated as opposed to only 20% of full time jobs which has left underemployment very high at 11.2%, most of the jobs growth seen in August was due to “sole traders” who may have been encouraged to return to the labour market due to the return of job search requirements for JobSeeker and the impending tapering of JobKeeper but who are not actually doing anything because hours worked barely moved in August and effective unemployment remains high at 9.5%.

August’s fall in official unemployment holds out the promise that it won’t get as high as the 10% we expected by year end, but we still see it rising to 9% as more people return to the workforce and as JobKeeper is phased down.

Dr Shane Oliver is Head of Investment Strategy and Chief Economist, AMP Capital